Insurance costs for auto, garage liability, EPLI and Workers’ Compensation (WC) continue to climb. For WC policies effective Sept. 1, 2025, the California Department of Insurance has approved a rate increase of about 9%. Other states are also in the same league. It is a good time to learn how premiums are calculated and how to reduce them.

Background

WC insurance is mandatory in the United States and many other countries. It ensures employees receive medical treatment and disability benefits for workplace injuries, while protecting employers by providing immunity from employee lawsuits for alleged negligence. WC premiums are paid entirely by employers and represent a significant, manageable business expense. Rate increases are attributed to significant increases in legal expenses (see the ads on the sides of the highways), rising medical and claims costs, more cumulative trauma claims and increased claim adjustment expenses.

Cost Containment

WC premiums are calculated using a base rate that reflects job duties, payroll size and the number of employees. This base rate is then adjusted by an experience modifier (X-Mod) that is directly tied to the frequency and severity of workplace injuries. Losses are calculated from claims paid by the insurance company, so every claim impacts your premium for multiple years. Preventing injuries is the most effective cost-control strategy. We assume you are running a lean operation with payroll expenses under control.

Proactive Steps

Reducing both injuries and claims starts with a proactive approach to safety and claims management. Employers should:

- Form and maintain an active safety committee.

- Designate an approved medical clinic. Seek a clinic approved by your insurance carrier and post details on your employee notice board.

- Encourage open communication.

- Document thoroughly:

- Accident investigation

- Employee statement of injury

- Employee counseling

- Declination of treatment by employee

- Verify coverage for contractors working on your premises, e.g., detail company, gardeners, etc. Get coinsured on their policies. Your WC policy covers only employees on your payroll!

Post-Claim Steps

- Promptly report all claims to the carrier — even declinations with signed forms. In California, the 90-day rule for workers’ compensation claims means that if the insurance carrier fails to accept or deny a claim within 90 days of it being submitted to the employer, the claim is presumed accepted. Any delay in submitting claims can result in claims being accepted by default, even the fraudulent ones, and they can cost you a pretty penny.

- Ensure supervisors investigate each claim and notify your carrier if legitimacy is in question. Flag the three Fs: frivolous, fictitious and fraudulent. If a third party is at fault, pursue subrogation.

- Offer modified duty, when possible, to reduce costs. If an employee denies a bona fide modified work duty offer, the insurance company can stop the payments on indemnity.

- Work closely with your claims adjuster by providing the requested information quickly for efficient claim handling.

Managing Claims

Stay actively engaged in the claims process — ask for updates frequently. Open claims with high reserves are a major reason X-Mods increase. Remember that legal expenses do not affect your X-Mod, but illegitimate claims should always be challenged. Sometimes settling quickly is more cost-effective than allowing claims to linger. For litigated cases, voluntary resignations may be part of the settlement strategy. The best claim is one that is prevented, and the next best is one that is promptly closed.

Calculating Costs

We used payroll data and losses incurred over a four-year period to calculate an employer’s workers’ compensation premium. For example, the 2025 X-Mod basis for policy renewal on Jan. 1, 2025, is WC claims from 2021, 2022 and 2023. Although claims from 2024 are excluded from the X-Mod calculation, they remain critical for underwriting. Even with a favorable or “credit” X-Mod, a dealership with multiple recent claims may be viewed by carriers as having a weak safety culture, which can lead to fewer quotes and/or higher premiums.

Before submitting data, ask:

- Is your payroll data correct? Payroll data for the service department that includes both technicians and service drivers will cost you. The risk for service advisors working behind computer screens in an air-conditioned office is significantly lower than that of a technician working in the shop, facing physical risks from moving machinery and heavy lifting; hence, a lower premium rate is applied to advisors. Ensure they are classified differently.

- Are X-Mods calculated correctly? According to insurance brokers, 75% of all X-Mods are incorrect.

- Are subrogated and joint claims included or missing?

Cost Savings

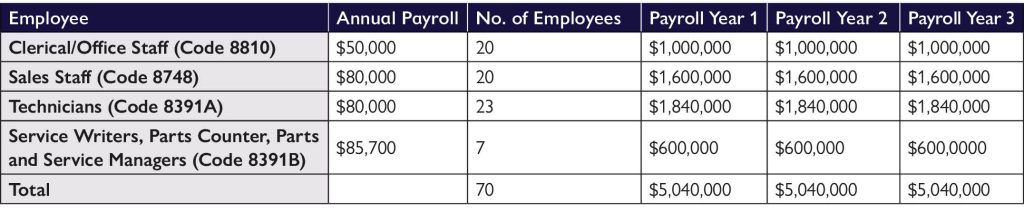

To illustrate insurance premium calculations (which may vary based on the difference in injury rates), hypothetical calculations were made for two employers, Employers I and II, who have the same payroll. On the next page, Table A shows the payroll data for each type of employee. Table B illustrates the excessive injuries of Employer I and Employer II. Employer II has four more injuries than Employer I, resulting in a total loss of $282,500, compared to a total loss of $45,004 during the same period. While the insurance company pays these losses, the difference between the two premiums is $174,540. A savings of $174,540 due to fewer injuries (Employer I, see Table C) provides a competitive advantage.

The fact that injuries affect the premium rate for three consecutive insurance years highlights the importance of preventing workplace injuries. Investing in time, training and equipment for employees is worthwhile, especially given the magnitude of premium savings described in our example. The benefits of being a caring and proactive employer in terms of employee productivity and morale are an important additional consideration.

Class Code 8391A vs 8391B (CA only)

- Class code 8391A applies to service technicians, porters and drivers. Any employee of the dealership who is engaged in repairs, maintenance, service, detailing or cleaning of automobiles or trucks should be assigned to this class code. Any employee engaged in driving or transporting automobiles or trucks should also be assigned to this code, as should parts drivers.

- Class code 8391B applies to service writers, estimators, parts managers, parts counter-persons and service managers.

Table A: Payroll Data (Employer I & II)

Table B: Injury Data and Losses Paid Per Injury

*Death benefits are statutorily limited in certain states. In California, death benefits are capped at $320,000. Only $175,000 is used in this sample calculation.

Table C: Estimated Premium Costs

Note 1: Wages and employee count for employees (CA automobile dealership) in Table A are fictitious and used illustratively.

Note 2: The Experience Modification in Table C utilizes California rates and formulas. Calculations for other states will vary.

Note 3: Table C premiums are before underwriter’s “risk adjustment” debits, credits or premium discounts (if any). A good safety record can earn you discounts from reputable carriers. Conversely, a poor safety record will result in increased premiums.

DISCLAIMER: Employers must consult with their WC insurance brokers for a better understanding of their WC premiums and safety consultants for matters related to safety. The contents of this article are for informational purposes only and are not to be considered as legal advice. The premium numbers are for discussion purposes, and actual numbers for X-Mod and premium calculations may vary on a case-by-case basis.

Sam Celly of Celly Services Inc. has been helping automobile dealers comply with EPA & OSHA regulations since 1987. Sam received his BE (1984) and MS (1986) in Chemical Engineering, followed by a J.D. from Southwestern University School of Law (1997). Learn more at www.epaoshablog.com. Your comments/questions are always welcome. Please send them to sam@cellyservices.com.